Asian currencies still on the straight and narrow

Non-Japan Asia (NJA) currencies have weakened in the past four weeks, led by sharp falls in the INR, THB and IDR (Figure 1). Rising oil prices and tepid exports are amongst the common factors behind this currency weakness.

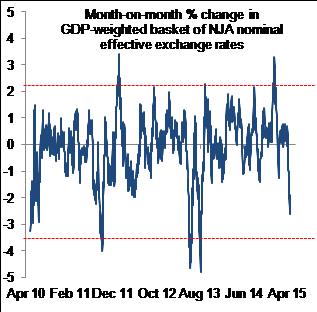

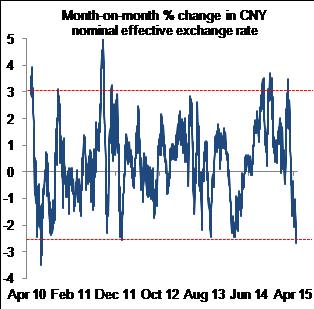

But precedent suggests that outside of periods of major financial shocks, these bouts of currency depreciation are reasonably shallow and short-lived and typically followed by similarly shallow and short-lived bouts of currency appreciation (Figure 2). It’s a similar picture for the CNY (Figure 3).

This pattern of mean-reversion reflects in part the ebbs and flows of foreign FX flows and seasonality of current account flows. Importantly, it also reflects NJA central banks’ willingness and ability to smooth the path of their currencies via FX (and verbal) intervention. They have to balance the competitiveness of their currencies and large export sectors on the one hand with imported inflation and the cost of servicing foreign-currency denominated debt on the other.

NJA exports and inflation have been soft in recent months, giving central banks both the incentive and the room to allow a modicum of currency weakening. FX debt in NJA remains modest both by historical and EM standards and is partly currency and earnings hedged but the increase in FX-denominated corporate debt and servicing costs, notably in China, does provide policy-makers with an argument in favour of a stable or mildly appreciating local currency. Furthermore, central banks of countries with historically volatile currencies – Indonesia for example – have come a long way in fading FX peaks and troughs.

I would therefore expect NJA central banks to be biased towards stability in their currencies, or even modest and slow appreciation, in coming weeks.

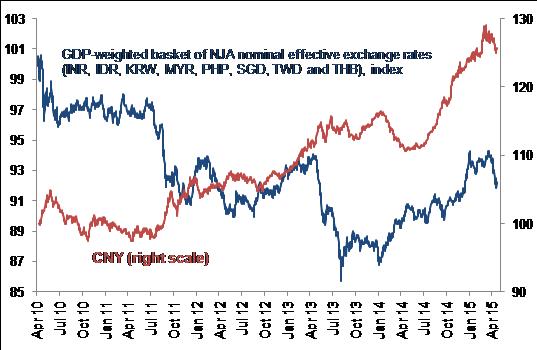

Figure 1: NJA currencies have weakened about 2% in the past month

Figure 2: But precedent suggests sell-offs (and rallies) are reasonably modest and short-lived…

Figure 3: …including for the CNY

Higher oil prices and soft exports removing some currency support

I estimate that a GDP-weighted basket of NJA nominal effective exchange rates (NEERs) has weakened about 2% since mid-April, and if the CNY is excluded is back near early 2015 levels (see Figure 1). While country-specific drivers have contributed to individual currencies’ weakening, a number of common factors can be identified, including:

- Rising crude oil prices: The 28% increase in international crude oil prices since mid-March and subsequent increase in the value of oil imports. The nature of crude-oil contracts suggests this price increase is likely to feed through to the USD-value of imports over coming months. As I elaborated in Crude Expectations (16 January 2015), NJA economies have significant net oil imports. The only exception is Malaysia which is a small net crude oil exporter.

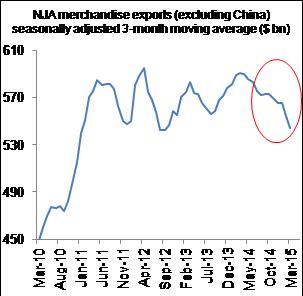

- Weak exports: The USD-value of exports from Asia (excluding China), seasonally adjusted, were down 8% year-on-year in March, according to my estimates, and this was not a one-off. Indeed, in Q1 2015, exports contracted 8% from Q1 2014 and 20% annualised from Q4 2014 (see Figure 4). The picture is similar in China (see Figure 5).

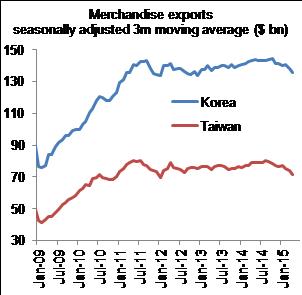

Furthermore, Korea and Taiwan have released April data showing the USD-value of exports at multi-year lows, according to my calculations (see Figure 6). The US dollar’s appreciation accounts for only part of the weakness in the USD-value of Asian exports. Figure 7 strips out these currency effects and is effectively an estimate of export volumes, which have flat-lined for the past 18 months.

Figure 4: Exports slumped in Q1 2015…

Figure 5: …including in China…

Figure 6: …and were weak in Korea and Taiwan in April

Figure 7: Export volumes have flat-lined for 18 months

Incentives for central banks to fade or even reverse currency moves

Precedent suggests that outside of periods of major financial shocks (e.g. 2008-2009), these bouts of currency depreciation are reasonably shallow and short-lived and typically followed by similarly shallow and short-lived bouts of currency appreciation (Figure 2). It’s a similar picture for the CNY (Figure 3).

This pattern of mean-reversion reflects in part the ebbs and flows of foreign FX flows and seasonality of current account flows – for example the rise in worker remittances to the Philippines in the run-up to Christmas.

Importantly, it also reflects NJA central banks’ willingness and ability to smooth the path of their currencies via intervention in the FX market and/or verbal intervention. They have to balance the competitiveness of their currencies and large export sectors on the one hand with imported inflation and the cost of servicing foreign-currency denominated debt on the other.

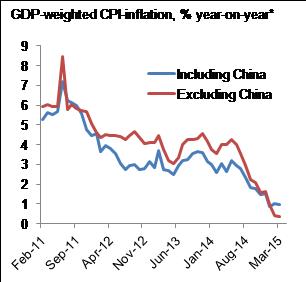

NJA exports have weakened in recent months, as detailed above, giving central banks the incentive to allow a modicum of currency weakening and support export competitiveness. Importantly, inflation has also weakened to multi-year lows (see Figure 8) which has given NJA central banks the room to maintain loose monetary conditions – i.e. low interest rates and weaker currencies.

Figure 8: NJA-inflation has fallen to multi-year lows

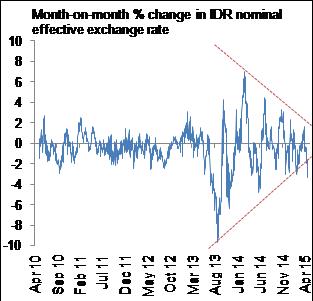

Figure 9: Volatility in IDR NEER has eroded significantly in the past 18 months

FX debt in NJA remains modest both by historical and EM standards and is partly currency and earnings hedged but the increase in FX-denominated corporate debt and servicing costs, notably in China, does provide policy-makers with an argument in favour of a stable or mildly appreciating local currency. Furthermore, central banks of countries with historically volatile currencies – Indonesia for example – have come a long way in successfully fading FX peaks and troughs (see Figure 9).

I would therefore expect NJA central banks to be biased towards stability in their currencies, or even modest and slow appreciation, in coming weeks. Underlying flows are unlikely to support rapid or sustained. Modest global growth and demand is likely to curb Asian exports while the uncertainty about the timing of Fed rate hikes may dampen FX inflows into Asia.

Olivier Desbarres currently works as an independent commentator on G10 and Emerging Markets. He has over 15 years’ experience with two of the world’s largest investment banks as an emerging markets economist, rates and currency strategist.

Sources

Fig 1 – www.olivierdesbarres.co.uk, Investing.com

Fig 2 – www.olivierdesbarres.co.uk, Investing.com

Note: Includes INR, IDR, KRW, MYR, PHP, SGD, THB and TWD

Fig 3 – www.olivierdesbarres.co.uk, Investing.com

Fig 4 – National statistical offices, www.olivierdesbarres.co.uk

Note: includes India, Indonesia, Korea, Malaysia, Philippines, Singapore, Taiwan and Thailand

Fig 5 – China customs, www.olivierdesbarres.co.uk

Fig 6 – National statistical offices, www.olivierdesbarres.co.uk

Fig 7 – National statistical offices, www.olivierdesbarres.co.uk

Note: the USD-value of exports is deflated by a GDP-weighted basket of NJA exchange rates vs the US dollar (includes INR, IDR, KRW, MYR, PHP, SGD, THB and TWD)

Fig 8 – National statistical offices, www.olivierdesbarres.co.uk

Note: Wholesale Price Inflation for India

Fig 9 – www.olivierdesbarres.co.uk, Investing.com