So much change – so little difference

Events, data and price action in recent days have provided much debate and if anything reinforce my view that volatility in asset prices is unlikely to be tamed any time soon (see Be careful what you wish for, 1 November 2016). The odds of Donald Trump winning next week’s US presidential elections have gone up, the probability of the UK opting for hard Brexit has come down, US data have been mixed and global yields and equities have come off. But ultimately I do not think the underlying picture has changed as much.

- Democratic candidate Hilary Clinton still has a 66% chance of winning the US presidency according to FiveThiryEight.

- The UK is still on course to leave the EU (albeit in the not so near future) which in turn is likely to cap Sterling’s recent rally.

- I still expect the US Federal Reserve to hike its policy rate at its next meeting on 14th December, in line with market pricing of a 70% probability of a 25bp rate hike.

- The Bank of England’s updated forecasts, if anything, have reinforced my view that it is unlikely to change its policy rate or QE program in the foreseeable future.

- Developed central banks have likely reached an important inflexion point with further rate cuts increasingly unlikely. That was certainly the Reserve Bank of Australia’s message at its policy meeting today.

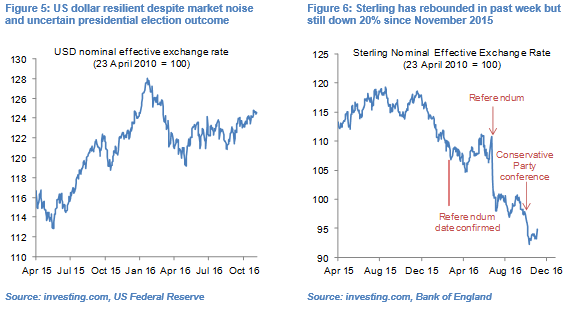

- The US dollar nominal effective exchange rate (NEER) has been resilient (see Figure 5) and I maintain my forecast that the dollar will post a third consecutive year of (albeit more modest) gains.

US presidential elections – Tipping points and limited use of national polls

News earlier this week of the FBI’s latest potential investigation of a new batch of emails from Hilary Clinton’s private server has certainly rattled markets (not to mention the Democratic Party). New national opinion polls are seemingly being conducted on hourly basis but they may not be of the greatest use.

For starters, they are pretty volatile, depending on the news of the day. Second, their margins of error are roughly as large as the lead which Clinton supposedly still has. But more importantly, they are not that useful because the US runs a first-past-the-post (“winner takes all”) presidential election in 50 states (similar in that sense to the general elections in the UK and very different to other presidential elections, such as in France for example).

So what matters is a candidate’s ability to win swing-states, even if by the smallest margins (conversely candidates do not even bother campaigning in sure-win states). Even a minuscule change in support for a candidate in a swing state can dramatically swing the probability of a candidate winning the necessary 270 electoral college votes and thus the overall election. Thus all the talk about “tipping points” and the importance of focussing on state-by-state polls, particularly where the vote is likely to be tight.

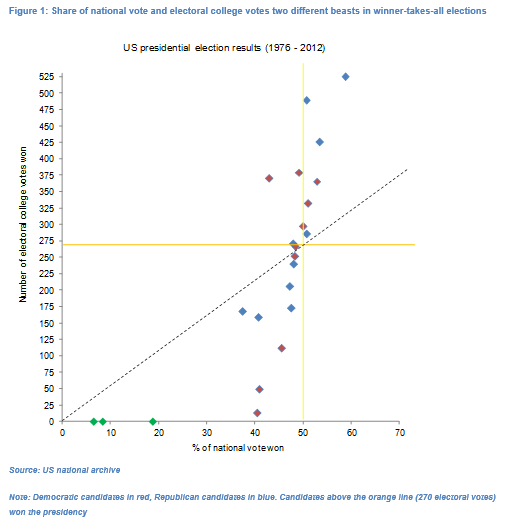

Figure 1, which looks at the share of the national vote won versus the number of electoral college votes won in US presidential elections since 1976, says it all really. In a Proportional Representation (PR) voting system, all US presidential candidates would have be on the dashed line. That’s rarely been the case (it was ironically in the fiercely contested 2000 election between Bush and Gore). To use an extreme example, Democrat candidate Dukakis got 45.6% of the national vote in 1988 but only 111 seats. Bill Clinton won only 43% of national vote in 1992 but more than three times as many seats (370 to be exact).

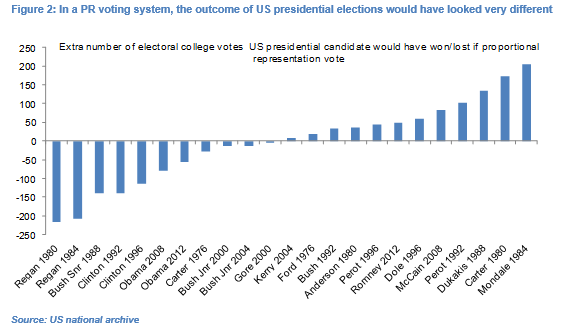

Figure 2 shows how presidential candidates would have fared under a PR system (for starters Gore, not Bush would have become President in 2000). It again highlights that national polls are only of marginal interest, particularly in tight races – which is the case between Trump and Clinton (of course in extreme scenarios where a candidate was polling 0% or 100%, national polls would tell us all we need to know).

Data and the Fed – a marriage finally made in heaven?

I noted in Be careful what you wish for (1 November 2016) that the rebound in US GDP growth in Q3 to 2.9% annualised, decent September macro data and higher international oil prices had in my view paved the way for a second consecutive December rate hike. Data since published have not fundamentally changed my view.

There is evidence that while growth in the services sector slowed in October (the ISM fell 2.3 percentage point to 54.8), the manufacturing sector is somewhat faring better: non-farm productivity growth rebounded to 3.0% qoq in Q3, the manufacturing ISM picked up in October and factory orders rose for the third consecutive month. This is important to a US central bank which has consistently referred to the prevailing weakness in the manufacturing sector.

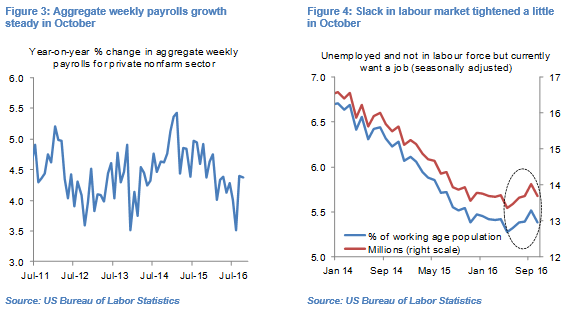

As important of course is the health of the labour market and overall today’s US non-farm payroll release for October was weaker than expected. It certainly fell short of convincing the rates market of the need to reprice higher the odds of a December hike. But digging below the surface, there was further evidence that the dip in growth of private sector aggregate weekly payrolls in August to 3.5% year-on-year (yoy) may have been a one-off. Indeed growth was steady in October at 4.3% yoy (see Figure 3). I view this measure as key as it incorporates estimates of average hourly earnings, average weekly hours and employment.

Moreover, the number of those unemployed and not in the labour force but looking for a job fell by 328,000 in October, reversing the rise recorded in September and arresting a four-month consecutive increase (see Figure 4). These numbers suggest that while the US economy is not at full employment, the slack in the US labour market remains modest.

High Court ruling puts British Parliament back in driving seat – albeit an uncomfortable one

The UK High Court ruled that, from a legal perspective, British Parliament, not the government, has the authority to trigger Article 50 – the Article of the Lisbon Treaty which officially sets in motion the two-year process by which the UK would have to leave the EU.

The government has confirmed that it would appeal the ruling in the Supreme Court, which is in turn expected to pronounce its decision in the first half of December. It is unclear at this stage whether the government would appeal to the European Court of Justice should the Supreme Court confirm that the government cannot legally trigger Article 50 (which in itself would be somewhat ironic given that one of the objectives of Brexit is to gain greater independence from the EU’s judicial system).

Perhaps this was not a totally surprising outcome. After all, the referendum was never legally binding, only advisory, as I had stressed in Europe – the final countdown (12 June 2016). The UK Parliament website had stated that: “The national result, once declared, will be final but it is not legally binding. The European Referendum Act 2015 does not include provisions to implement the result of the referendum; legally, the Government is not bound to follow the outcome. However, it would be very unlikely for the Government to ignore the outcome of the referendum”). Theresa May has a popular mandate to leave the EU (albeit by a small margin) but no clear mandate on the terms and conditions of the UK’s exit and no legal mandate to bypass Parliament.

Assuming the Supreme Court upholds the High Court’s ruling (which legal experts think is likely), the government will have to push through legislation granting the House of Commons a vote on whether to trigger Article 50. Legal experts believe that this legislation is more likely to be primary legislation, not just a non-amendable motion, which would require approval from both the House of Commons and House of Lords and which based on precedent could be a lengthy and complex process. There will be Committee scrutiny that will prompt studies, the House of Lords, which was pro-Remain in the run-up to the referendum, will make recommendation and revisions will likely be put forward. This could tie up legislation almost indefinitely and it certainly make it less likely that Article 50 will be triggered by March 2017 – the deadline Theresa May has so far steadfastly stuck to.

Tactically messy, strategically smart?

On the surface, Prime Minister Theresa May’s credibility has been further dented. Assuming that the Supreme Court upholds the High Court’s ruling, she will have lost her battle to control the procedure and timeline by which the UK leaves the EU. In the process she has alienated a large swath of her own Conservative members of parliament (MPs), who are in either in favour of the UK remaining in the EU or leaning towards a softer form of Brexit. At the very least her stance of keeping MPs at arm’s length, her decision to appeal the High Court’s decision and her open criticism of Bank of England (BoE) Governor Mark Carney have raised serious questions of the government’s respect for the country’s executive and judicial bodies.

However, what she has gained – time and a possible route to soft Brexit – may outweigh what she has lost. She will have known that if the onus is on Parliament, which now appears will be the case, there is a fair chance that Article 50 will not be triggered by March 2017 given the potentially lengthy process of passing primary legislation which I describe above. At the very least, this buys the government more time to negotiate the outlines of a deal with the EU while Theresa May can still claim to respect the will of the electorate which voted by 52% to 48% to leave the EU in the June referendum.

Moreover, in this scenario there is a greater probability that the UK will opt for a softer form of Brexit – which maintains the UK’s access to the Single Market or at least Customs Union – rather than hard Brexit. This may appear to run counter to Prime Minister May’s preferred route but let’s not forget that in the run-up to the referendum she had adopted a largely pro-EU stance and there were certainly no signs that she favoured hard Brexit[1]. At the same time, in the run-up to the EU referendum about 470 of the 650 MPs, or 70%, expressed a preference for the UK to remain in the EU with fewer than a quarter being pro-leave.

So while there is no precedent for the House of Commons voting against the result of a referendum, it is conceivable that MPs will delay a vote on Article 50 until they both have greater clarity about what the UK can negotiate with its EU partners and are confident that a soft version of Brexit is on the table. As I argued in Post referendum circular reference (7 July 2016), Parliament will not want to kick start an almost irreversible process whereby the UK has announced a divorce but does not know the terms and conditions of this divorce, let alone what its new relationship will look like. This time delay could again be lengthy as negotiations with EU leaders are likely to take place behind closed doors (EU leaders have repeatedly stressed that officially they would not discuss the details of the terms and conditions of the UK’s divorce from the EU, let alone of its new its new arrangement with the EU, until the UK has triggered Article 50).

The bottom line is that the triggering of Article 50 is unlikely to happen any time soon and if it does, soft rather than hard Brexit is likely to be the end goal, in my view. MPs could claim that they are both respecting the will of the people (to leave the EU) but are also doing what they think is best for the country (to maintain the UK’s access to the Single Market or at least the Customs union).

Sterling rebound – everything is relative

Much has been made of Sterling’s rally in the past 24 hours. Currency markets have seemingly interpreted positively the possibility that Article 50 may not be triggered or at the very least that it will be delayed until soft Brexit is on the table. This caps off an eight-day streak which has seen the currency’s NEER appreciate 1.4% thanks to stronger-than-expected Q3 GDP growth, a stronger-than-expected jump in the services PMI in October, Nissan’s decision to keep its UK plant and BoE Governor Carney’s decision to extend his term to 2019.

But as Figure 6 shows, this rebound needs to be put in perspective, with the Sterling NEER still down 20% since November 2015. Moreover, while I have argued that the probability of soft Brexit has likely increased, there is still a great deal of prevailing uncertainty as to if, when and how Parliament may ultimately vote and what they will be voting on. This uncertainty is unlikely to dispel near-term, in my view, which is likely to weigh on foreign FX inflows and in turn cap Sterling gains.

Moreover, there has been renewed talk of an alternative scenario whereby Theresa May would call early national elections. This could happen via three routes, neither of which is likely in my view and Theresa May has so far ruled out early elections. But again this uncertainly is likely to act as a headwind to a sustained and more potent Sterling appreciation.

- A two-thirds majority vote by parliament – this is a high threshold which would require the majority of MPs from the ruling Conservative Party and opposition Labour Party to vote in favour of early elections, which may in turn see either or both parties losing seats.

- Theresa May calling for a motion of no-confidence in her own government which would require a simple majority. This could backfire embarrassingly as the ruling Conservative Party only has a small majority of 11 seats.

- Repealing the Fixed Term Parliament Act.

Olivier Desbarres

Olivier Desbarres currently works as an independent commentator on G10 and Emerging Markets. He has over 15 years’ experience with two of the world’s largest investment banks as an emerging markets economist, rates and currency strategist.

[1] I would argue that she has pushed for hard Brexit for mostly tactical reasons. In the unlikely event of the EU having caved in and agreed that the UK could still access the Single Market but still control immigration she would have been feted. In poker terms, she had a weak hand and there was no upside exposing it early on in the negotiating game.